IMPLEMENTATION OF THE NEW LUXURY TAX ON BOATS

The federal government implemented the new luxury tax on boats on September 1, 2022.

Therefore, all boats (2019 and older) that will be sold from September 1, 2022 will be taxable, even if the purchase contract was signed at the dealership well before this date (during the year 2022).

The notion of new or used boats subject to the new tax is a little nuanced for sales made by a dealer; time and case law will tell us more in the coming weeks. But one thing is certain, the new boat from 2019 is definitely included.

However, it appears that contracts signed before December 31, 2021 are exempt, regardless of the time of final delivery. But the registration of the boat under Transport Canada must have been done before September 1, 2022 in order to avoid taxation upon resale, even if it is a sale between individuals. Therefore any boat registered after September 1, 2022 may be subject to the luxury tax, even if it is a sale between individuals. Everything needs to be checked…

According to available information, this new tax will be applicable to both new and used boats (for 2019 and above) over $250,000 CAD sold by dealers, but boats already registered in Canada or elsewhere (before September 1, 2022). will not be included for this new tax for a sale between individuals or via a broker.

Therefore the sale of a boat between individuals is not subject to this new luxury tax if the boat has already had an owner before September 1, 2022.

This rule must be interpreted as follows (subject to):

1- So in general, a boat will not be subject to this new luxury tax if it is currently in Canadian territory or elsewhere (US or EURO) as part of a sale between individuals with or without a broker, but it must have been registered (registered) before September 1, 2022.

2- So a boat acquired and registered in Canada or elsewhere before September 1, 2022 and sold thereafter will be excluded from this new tax as part of a sale between individuals.

3- A boat acquired after September 1, 2022 and which has a serial number of 2019 and above, the owner therefore pays the luxury tax when purchasing it from a dealer. Upon resale, the next owner will or will not be subject to this new tax given the

rule #1. The resale of a boat registered after September 1, 2022 may be subject to luxury tax, certain criteria must be verified.

4- So for boats acquired after September 1, 2022, the luxury tax is payable by the first owner who registers the boat in Canada. See rule 7.

5- A boat acquired outside Canada and which enters Canada after September 1, 2022 must demonstrate that it has already been registered elsewhere in the world before September 1, 2022 (having already been owned by someone).

6- A boat acquired outside Canada and which remains outside Canada continues to benefit from a Canadian tax exemption regardless of the date of manufacture, in other words, the current situation remains unchanged for this situation.

7- The luxury tax is payable only once for the same boat.

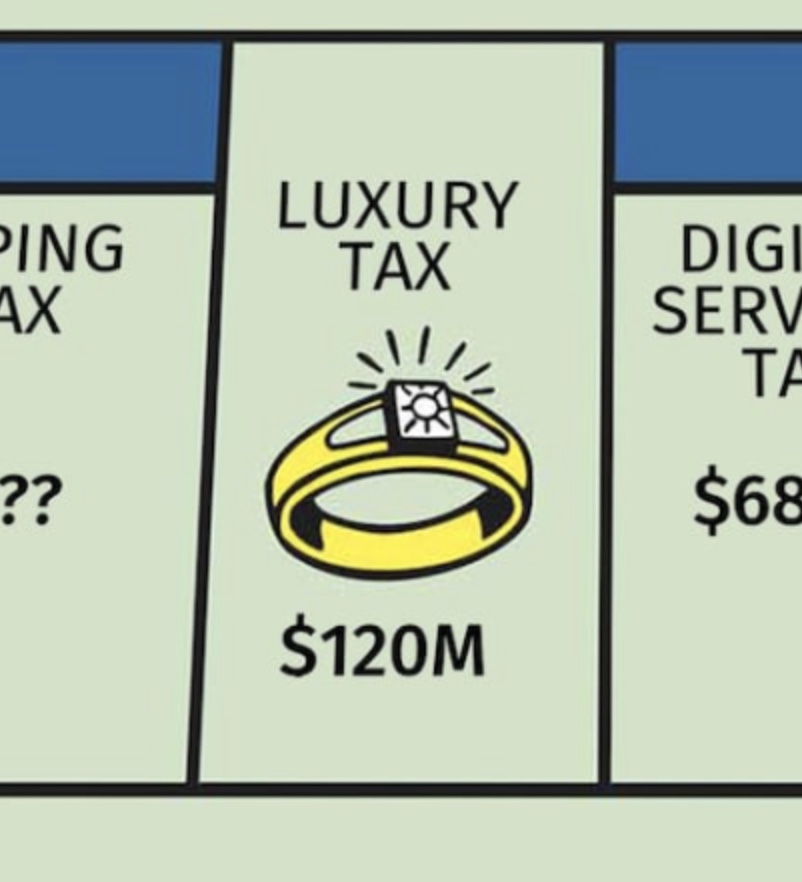

You have the choice between 10% of the total value of the contract or 20% of the excess of $250,000, you take the smaller value between these calculation methods.

Don’t forget that GST and QST apply to this new tax. So it’s a tax on existing taxes.

In addition, if you import a boat into Canada, it must respect the various free trade treaties in force with certain countries, otherwise a customs rate of 9.5% is applicable.

We are awaiting details on the terms of application, it is always the finer details that are important.

The brokers at Ita Yachts Canada remain on the lookout for you, so all boats from 2019 and above are included for the moment in this new tax.

For a detailed explanation, see this PODCAST by clicking here.(French only)

Follow this link for a complete section published by the Government of Canada about this new luxury tax.

Views: 1440